Ted Spradlin

Ted Spradlin

Fix-and-Flip Financing: What is Gap Funding?

If you’re a house flipper already approved for a hard money first mortgage, but need a second mortgage to cover down payment and closing costs,...

This question has come in through the website dozens of times over the years from prospective house-flippers who are short on funds to close their transactions. What they’re asking for is something called “gap funding,” which is a hard money second mortgage that “fills the gap” when they need funds for down payment and closing costs.

PLEASE READ:

FCTD does not originate stand-alone second position "gap funding" loans behind a high-leverage fix-and-flip loan. The risks are too high, far outweighing the reward, which I’ll go into below.

This blog post will break down a recent request we received from a house-flipper, who purchased a fixer-upper for $480,000 and requested a second trust deed to cover down payment and closing costs. I’ll cover all the aspects that a borrower would need to know before continuing down this path, including:

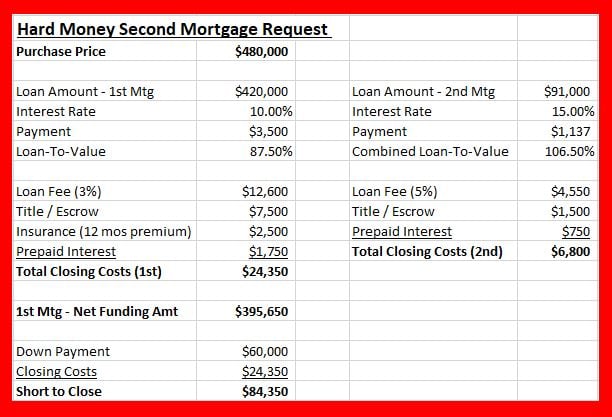

To start off, below is a summary of the loan request for the hard money second mortgage:

“Another lender approved me for a first mortgage of $420,000 without any rehab funds on a $480,000 purchase. The rehab budget is $75,000 and will take about 3 months. I’ll pay all rehab fees out of pocket. The After Repair Value is $650,000. I need a second mortgage for the down payment and closing costs. Close of escrow is in 5 days. Please call me immediately.”

There are a few things that immediately caught my attention:

87.50% Loan-To-Value (LTV) on the first mortgage:

The LTV loan commitment makes me think financing is probably coming from an institutional fix-and-flip lender that sells these loans off to Wall Street or other fixed-income investors. I’m certain that they don't allow a junior lien (more below).

No money to bring in for down payment and closing costs:

Is that because the borrower is inexperienced? I doubt it, because the lender offered 87.50% LTV. Do they have other projects that are delayed? If so, are they overleveraged across their projects? Are they in default or at risk of default? Overleveraged and/or defaulted borrowers sometimes avoid disclosing other projects in progress or in default. We can find out through a quick background check, since hard money loans aren’t reported on personal credit reports.

Close of escrow in 5 days:

If we chose to move forward, we would be under the gun to act on a scenario that would require significant due diligence since this borrower is brand new to FCTD. I would order an appraisal, and request tax returns, bank statements, schedule of real estate with all mortgages, and a credit report. I would also run a background check to look for foreclosures, judgments, liens, financial convictions, tax liens, etc. Plus, we’d need to work with the first lienholder on an Intercreditor Agreement so that the second lienholder would be notified if the borrower defaulted on the first mortgage (very important!)

Let’s discuss this in more detail.

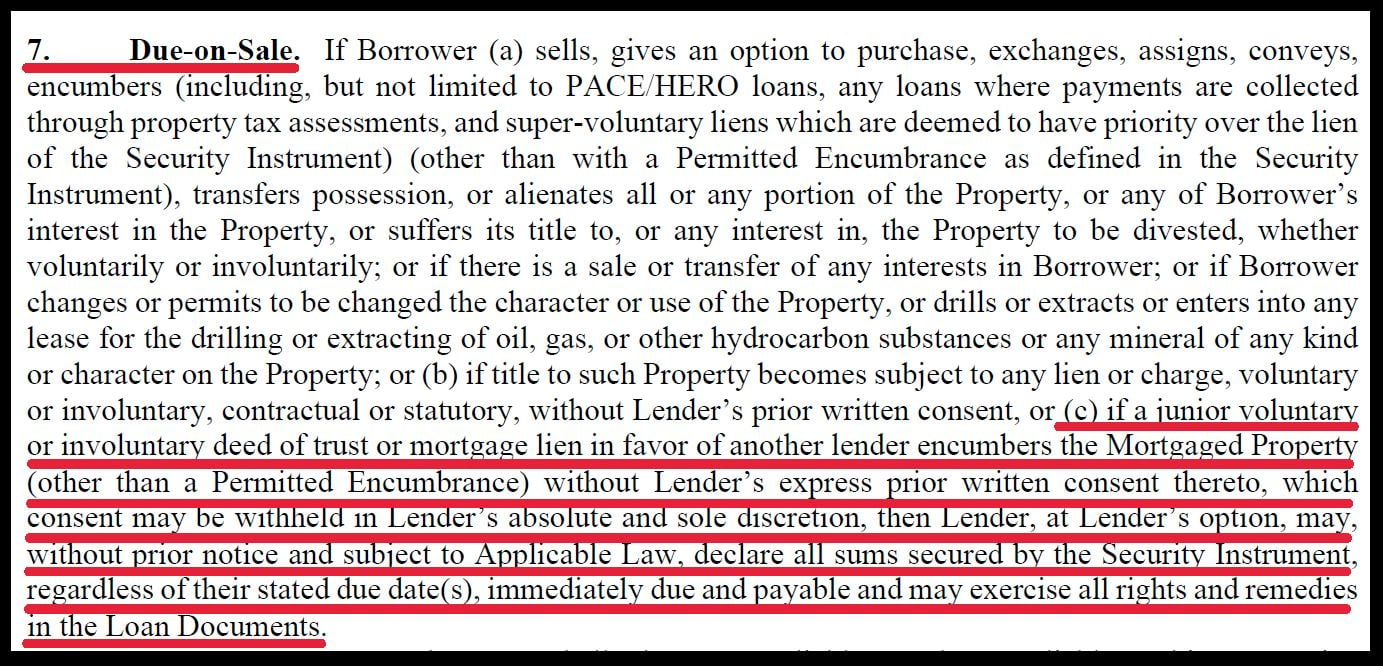

The first thing to do is ask the first mortgage lender for a proposed version of the Note to see if there is any “due on sale” language prohibiting a junior lien to be recorded on title. As I mentioned in #1 above, I suspect the $420,000 loan commitment to the borrower came from an institutional fix-and-flip lender that originates and sells loans immediately to a secondary market investor. FCTD works with several institutional lenders, and the loan documents are streamlined with “due-on-sale” language that doesn't allow a junior lien on the property.

Here’s an example of due-on-sale language regarding junior liens from the Note of an institutional lender:

There is no way that the institutional lender would allow a hard money second mortgage to close concurrently. They wouldn’t be able to sell the loan to the secondary market investor and would instead either need to carry it on their warehouse line or sell the loan at a discount.

Let’s say the first mortgage did allow junior liens, and you could find a trust deed investor willing to do a very high-leverage second mortgage behind an already high-leverage first mortgage.

What would the terms of a second mortgage look like?

In the example above, I used a cost of 5 points at 15.00% but I think for this level of risk, it could be more.

You might wonder why I made the second mortgage balance $91,000 rather than $60,000. It’s because the first mortgage lender will “net fund” the loan, excluding their 3% loan fee. Then, you have the other closing costs, title and escrow, 12 months of insurance premium, and prepaid interest on the mortgage. That comes out to $24,350, which would have to be absorbed by the second mortgage holder on top of the $60,000 down payment. The second mortgage will also have loan fees and closing costs from title and escrow, which gets us to a $91,000 loan amount.

Between both loans and standard closing costs, the borrower is looking at $31,200 in closing costs with very expensive financing.

This is where you need to think like a lender. As a borrower in this scenario, you go in optimistic that you’ll rehab this property within 2-3 months and get a full price offer after a week on the market, netting $50,000 profit in a few months. In this scenario, the lender will make their 5 points ($4,550) plus 4 months of interest ($4,550).

As a lender, or a mortgage broker who has been around 20+ years, we think the opposite. We calculate what it would cost in the event of a default — not just on the second mortgage, but on the first mortgage. Usually, if one loan is in default, the other is too.

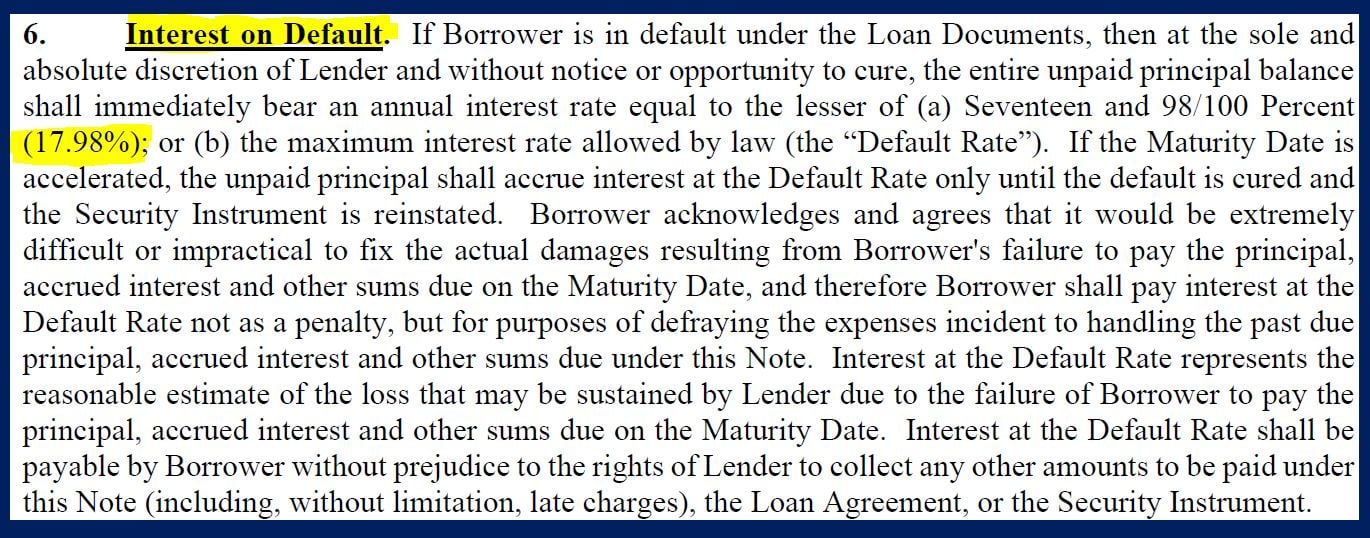

Private money fix-and-flip loans usually have late charges of 10% and a default interest rate from 15.00% to 24.00%, which kicks in after the 10-day grace period for the monthly payment.

I mentioned above in #3 that if I could find a second mortgage for this scenario, I’d need to work out an Intercreditor Agreement between the first and second lienholders. This is where it comes into play.

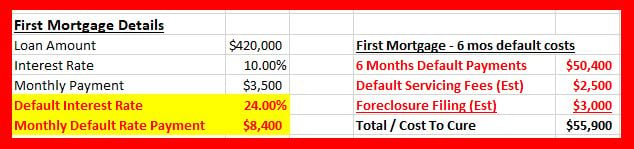

If our borrower defaults on the first mortgage of $420,000 with a $3,500/mo payment, they trigger a late fee of $350 and a new default interest rate of 24.00%, resulting in a $8,400/mo payment. (I used a default interest rate of 24.00% to make it scarier.)

The first lienholder will notify the second lienholder of the default. Most likely, the second mortgage will also be in default and the second lienholder will file a foreclosure action, which can take 3-6 months, depending on the property state. The first lienholder will probably file a foreclosure action as well, resulting in two concurrent foreclosures progressing at the same time.

While the second lien is working toward a foreclosure sale to close out the $91,000 junior position, the first mortgage balance — if still in default — is growing by nearly $10,000 per month with the late charges, the $8,400/mo default payment, and accruing foreclosure fees.

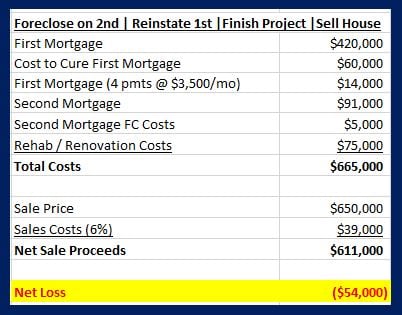

Let’s say the second lien forecloses in six months, which means the delinquent first mortgage balance grew from the original $420,000 to $480,000. The second lienholder can either pay off the entire first mortgage for $480,000, service the debt at $8,400/mo (remember — the first mortgage is still in default), or cure the default for approximately $60,000 to bring the interest rate back down to 10.00%, with a $3,500/mo payment until the property sells.

Below, I use the option where they cured the first mortgage default for $60,000:

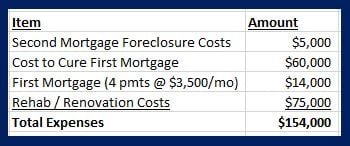

Now that the second lienholder has title with the first mortgage delinquency cured, it’s time to finish the rehab project, which came with an initial $75,000 budget. Hopefully, the home is in good condition and the contractors and supplies are readily available to complete the project and sell the house for the $650,000 target price.

To salvage that $91,000 second mortgage, the second lienholder will have to spend an additional $154,000, bringing their total outlay up to $245,000 just to get the house ready to sell.

Hopefully, the second lienholder-turned-house-flipper didn’t run into any unforeseen delays in completing the project. If they can sell for $650,000, they’d recoup some of the $154,000, but would still wind up with a $54,000 loss prior to pursuing a deficiency judgment against the borrower, who would have signed a Personal Guaranty in the loan documents for both loans — even if the loan was made to an LLC.

All of this time, energy and money was spent to salvage a $91,000 initial investment, netting a $54,000 loss! It’s hard for an experienced trust deed investor to take the plunge with an investor who is new to them.

As you can see, gap funding — a hard money second mortgage to cover down payment and closing costs — is incredibly risky (expensive) for a trust deed investor if things go sideways. If you already have financing in place with a high-leverage first mortgage lender like an institutional fix-and-flip lender, you’ll need to confirm that their loan allows for junior liens.

Most every trust deed investor FCTD works with won't do these loans in this structure. I’ve written more about gap funding, including some other ways you could go about getting the financing secured on a fix-and-flip project.

If you’re a house flipper already approved for a hard money first mortgage, but need a second mortgage to cover down payment and closing costs,...

First Capital Trust Deeds (FCTD) does not offer hard money second mortgages for personal debt consolidation, even to bring up credit scores in order...

If you’re trying to estimate the costs for a hard money second mortgage, we've got you covered with this blog post on pricing, closing costs, terms...