Borrower Inexperience or Over-Indebtedness

The weaker the borrower on paper, the higher the pricing for a private money loan – including a higher interest rate and upfront points. Signs of borrower weakness include:

- Borrower Inexperience

Borrowers with less experience will often have a higher cost of funds – without a track record of successful projects, they’re a riskier bet. - Low Credit Scores (650 and below)

A 650 FICO score usually indicates on-time payments, but most revolving accounts (credit cards) are maxed out or close to it. - Recent Bankruptcy and Foreclosure Activity

Multiple bankruptcy filings and foreclosure activity limits the number of hard money lenders willing to consider the loan. History has a way of repeating itself and most lenders don’t want to deal with likely legal action. However, there are some lenders who are open to working with those who’ve experienced bankruptcy and foreclosure. They charge a lot more for their money in anticipation of possible legal work down the road.

Property Condition

If the property is in rough shape – like being boarded up for a decade – the project would be expected to take longer due to unexpected repairs. This poses a higher risk of default to the hard money lender.

Leverage – Loan-To-Value (LTV) and Loan-to-Cost (LTC)

Higher LTV (75%+) and LTC (80-85%) loans cost more than lower-leverage loans at 50% LTV/LTC. The reason is less protective equity in high-leverage loans.

Availability of Capital – 5 Different Types of Funding Sources

If a borrower has several blemishes on their credit and background, they’ll be limited to local lenders with higher pricing. If they had a clean track record, they could obtain financing with one of the nationwide private lenders.

For example, FCTD secured a 10-house construction loan for a home builder who took on more projects than they could handle. The builder was unwinding and liquidating the other projects, which had gone into default. As a result, the nationwide private money construction lenders, (which had a lower cost of capital) would pass (3 points at 8.75%). We had to go with a local lender (5 points at 11.00%) to finance the construction.

Nationwide lenders usually have better pricing than local lenders.

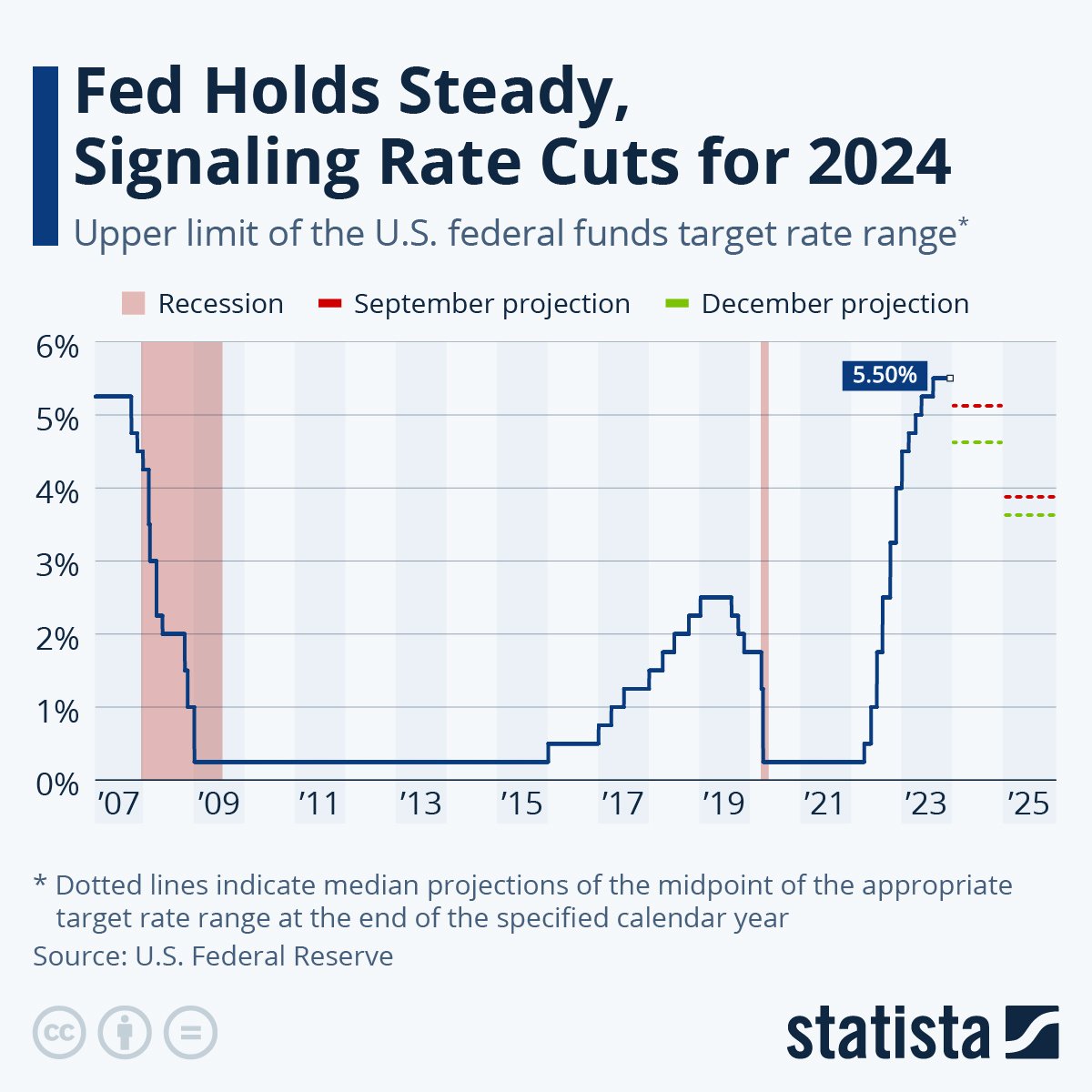

Federal Reserve Interest Rate Hikes

When the Fed started raising interest rates in March 2022, jumping from 0.25% to 5.50% in 16 months for the Federal Funds Rate, hard money and private money lenders followed along and raised their interest rates.