Ted Spradlin

Ted Spradlin

Trust Deed Investment – Multi-Lender Loans

First Capital Trust Deeds (FCTD) originates loans with trust deed investors in a few different ways. Most private money loans are funded by a single...

There are many pros and cons of trust deed investing. It could be the right move for you, especially if you want to seek out alternative investment opportunities in addition to stocks, bonds, and real estate. It could also be the wrong investment for you if the disadvantages outweigh the advantages for you and your investment goals.

This blog post will cover the pros and cons of trust deed investing, covering the following topics:

PROS:

CONS:

Before We Start – I'm Biased Toward Trust Deed Investing

Before I dive into the pros and cons of trust deed investing, I want to address my bias. Private money lending and trust deed investing has been my business for the past ten years and of course I’m going to be biased in favor of trust deeds. Yet, I’m realistic that it’s not for everyone and for those funding loans, trust deeds are just part of their investment portfolio, checking the box for fixed income.

Since co-founding First Capital Trust Deeds with Brett Everett in 2013, the company has closed over $2 billion in private money and bank loans for real estate investors, including $360+ million funded by individual trust deed investors. The real estate market has appreciated nearly every year, so investors could always count on the borrower either selling or refinancing into a rising market, which helped make trust deed investments more popular than they had been in decades past.

Going forward, market conditions can change and we all remember the Great Financial Crisis of 2008, where liquidity largely froze across the system, leading to the real estate values plummeting. I don’t expect another 2008, but I also don’t expect to see 20% annual price appreciation to make us look smarter than we really are any time soon!

On to the story….

Trust deeds can earn you a great return on investment (ROI) and can perform better than other asset classes. In times of volatility in equities, the steady yields of trust deeds from 7.50% to 13.00% can provide the only gains in your investment portfolio.

Due to the way the terms are structured, you receive monthly payments. The investment is considered a fixed security because of this feature. You have an income producing investment that is connected with the actual real property. When you have are looking for diversification among your investments, consider how trust deeds would work to satisfy an income producing segment.

There is going to be some volatility in your portfolio; however, you can dilute this by having diversity in your investment choices. One way is to fund trust deeds in different real estate markets. Another way is to invest in multi-lender, or fractional loans, where you are investing in many loans with other investors rather than just a handful of whole loans.

All trust deeds are secured by real property. If the borrower defaults on the loan, your funds are secured with the real estate collateral that you can initiate the foreclosure to get your money back. Ideally, lenders and borrowers want to avoid foreclosure, working out a payment or loss mitigation agreement allowing the borrower to bring the payments current or pay off the loan entirely through a property sale or refinance.

Not only are trust deeds secure, they are stable and predictable as long as you’re carefully underwriting the loan and not overleveraging the property. The interest rate and monthly payments are usually the same throughout the duration of the loan, allowing you to budget your income or reinvestment strategy.

FCTD works with a dozen or so trust deed investors who fund loans through their self-directed retirement accounts, 401Ks, IRAs, or pension plans they manage through their business. Some investors like lower yields (6.50% to 8.50%) when it comes to their retirement account while others who are in their forties and early fifties are aiming for higher yields from 10.00 to 12.00%.

I’ve owned rental properties in the past and it’s not for me after having a few destructive tenants. When I’d inspect the property, I couldn’t help but think, “Did your mom not teach you how to clean up after yourself?” I don’t like to deal with other people’s messes and I’m not handy, so I don’t own rental properties. Let someone else do that!

With trust deeds, you do your due diligence on the loan, fund the loan, and let the broker (FCTD) set up loan servicing for you, then wait have payments electronically deposited into your account each month. It’s a much easier process than being a landlord and managing your own properties.

Now, if you’re handy and highly skilled at working on houses, then being a landlord could be ideal for you. I admire people with those skillsets.

With every investment, there is some degree of risk. If you have done a careful analysis of the borrower and value of the real estate, you should be able to determine if you think this risk is too great. There are certain inherent risks and there are some you may not have considered. Fortunately, most of these can be avoided with the right strategy.

If you are considering trust deeds as an addition to your portfolio, it’s good to have some basic knowledge about real estate. You don’t need to be an expert, but you need to understand the state of the market in the city where the property sits. You should be able, with some research, to make an educated guess on whether the property and new development are sure to see gains or losses. A private money mortgage broker can help you assess those risks with all of the knowledge that their experience brings.

Risks can be mitigated as much as possible with proper due diligence, but it’s a good idea to look at any investment for its pros and cons.

Trust deed investments are not insured by the FDIC or any other government agency. Moreover, you will not have any guarantee that the investment will yield a positive return.

During the underwriting process, an Appraisal, Broker Price Opinion, or Desktop Valuation is completed. Most appraisals and valuations are very accurate. I have seen appraisals over the years where the value is clearly inflated, which I see the most with commercial buildings. Those inflated valuations are red flags and they usually correspond with the borrower wanting to pull a large amount of money out of the property, which would put the lender, or trust deed investor, in a bad spot where they’d lose their equity cushion between loan amount and market value. FYI – we pass on those loans every time.

The other way appraisals can’t guarantee value is that they’re backwards looking, usually going back 3-6 months rather than looking forward at expected values.

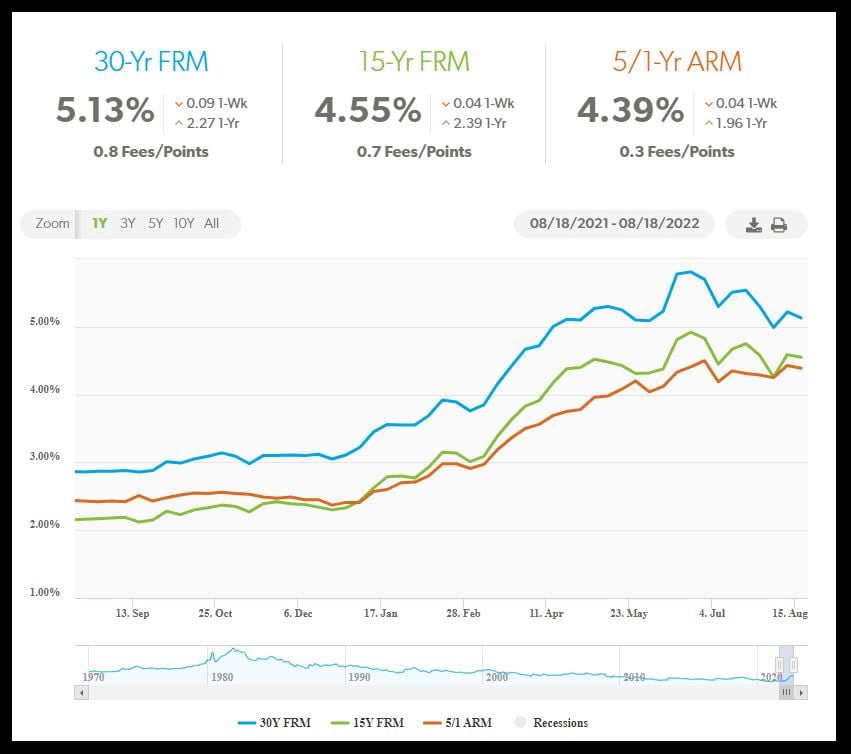

As I write this in August 2022, I’m still seeing appraisals using comparable sales from February and March of this year prior to interest rates nearly doubling in the conforming loan market from the low 3.00% range to nearly 6.00% in June and July (see the chart below). Buyers at the beginning of the year could afford to finance more debt at 3.00% and pay a higher price than they can today. Appraisals cannot predict where home prices will go based upon mortgage rates. But, every experienced trust deed investor I talk to, is working from the expectation that values will flatten or fall due to rising interest rates (and other factors).

When the loan is originated, it’s assumed that the borrower will make on-time payments for the duration of the loan. Sometimes they don’t make payments. In rare occasions, borrowers will be a first payment default which we’ve experienced in foreclosure bailout loans and divorces in progress. Most every loan performs to maturity or until paid off. There are the occasional delinquencies and occasional foreclosures filed, but that has been very rare.

On the flip side, some experienced trust deed investors like when the borrower defaults because default interest kicks in taking the rate up to 18-24% along with other default penalty fees of 10% of the payment. FCTD has an investor who will buy defaulted loans from mortgage funds looking to move non-performing loans off their books.

When COVID first hit in March 2020, the country shut down and nobody knew what was going to happen with life and business. Would it be another Black Swan, a phrase I first heard reading Taleb’s book of the same name? (My biggest takeaway from that book is that everyone in financial markets is very stupid except for him). Or, would it be massive fiscal and monetary intervention that would send asset prices higher and higher after the initial decline?

History gave us the latter.

Stimulus plus supply chain issues and the war in Ukraine have given us the highest inflation since the early 1980s and The Federal Reserve raising interest rates to slow inflation.

The only thing I’m certain of is that there will be shocks and surprises that will impact asset prices and markets, including real estate and the secondary credit market, where many private money loans eventually wind up.

Let’s say you fund a $700,000 fix and flip loan for a real estate investor acquiring a $1,000,000 fixer upper that they intend to spend $150,000 renovating and reselling for $1,500,000. As the lender, your gain is only the yield on the $700,000 loan @ 9.00% ($63,000). Whereas the borrower is looking at a $350,000 gain before factoring in debt service, insurance, utilities, and selling costs.

The real estate investor had to be at the job site, work with contractors, suppliers, supply chain delays, slow permitting timelines, building inspections, and all the other issues that come up with real estate projects.

If the trust deed investor does it right, they put all the heavy lifting onto their mortgage broker (shameless plug for FCTD) which has excellent people on staff and systems in place to execute every facet of the private money loan, including:

When the loan pays off, your money stops earning interest. This can be a problem for some investors who rely on mortgage brokers to provide them with funding opportunities because the money may sit idle for 30-60 days before the right opportunity is presented. If this happens a few times each year, that can be cut into the ROI.

There are two options:

1. Work with a broker like FCTD that has a high volume of loan opportunities each month. Sign up for our new online portal where you'll receive loans to either fund through the close of escrow or buy whole notes or fractional notes.

2. You could invest in a mortgage fund where your money is always working and you don't have to worry about or manage the idle periods when loans are paid off. If this is of interest to you, please let us know and we'll make introductions to a few excellent fund managers we work with.

Conclusion to Pros and Cons of Trust Deed Investing

If the pros of trust deed investing outweigh the cons, then we should have a conversation about funding private money loans for our borrower clients. If the cons resonate more with you, then I’ve done my job! Trust deed investing isn’t for everyone and there are other investments that can work just as well.

For those who want to move forward, please connect with Brett Everett – brett@fctd.com 619-414-2999.

First Capital Trust Deeds (FCTD) originates loans with trust deed investors in a few different ways. Most private money loans are funded by a single...

If you’re researching trust deed investments or looking to fund or buy existing Notes from new mortgage brokers, you’ll want to know if the rate of...

If you’re in the research phase of trust deed investing, you are probably looking online, talking to mortgage brokers and to friends who have...